If you run a business, it’s important to understand the current UK tax brackets for 2024. Doing this helps you manage your finances effectively. The UK’s tax system might seem complicated, but knowing the income tax rates and tax thresholds can make tax calculation much easier. This guide will break down the UK tax brackets, showing you how much you need to pay and why.

Whether you’re concerned about income tax, capital gains tax, or national insurance contributions, we’ll cover all the bases. Knowing the specifics of UK income tax rates helps you plan better and avoid surprises when you pay tax. We’ll also explain the different tax rates and how they apply to various income levels.

By the end of this guide, you will understand the UK tax brackets and feel more confident about your tax responsibilities. We’ll demystify the numbers and calculations, making it simple for you to navigate through the tax system. Let’s dive into the details and take the confusion out of understanding your taxes.

Need reliable professional assistance? Sleek offers cost-efficient accounting and tax compliance solutions in the UK, simply make and enquiry or share your requirements and get an instant quote. Our seasoned experts will help you and your business maximise returns and stay tax complaint without any hassle.

What are the current UK tax brackets?

Making money in the UK? You’ll want to get a handle on the current income UK tax brackets and rates. Knowing this helps you plan your budget better and dodge any nasty surprises when taxes are due. All three tax rates and thresholds are unchanged from 2023/24.

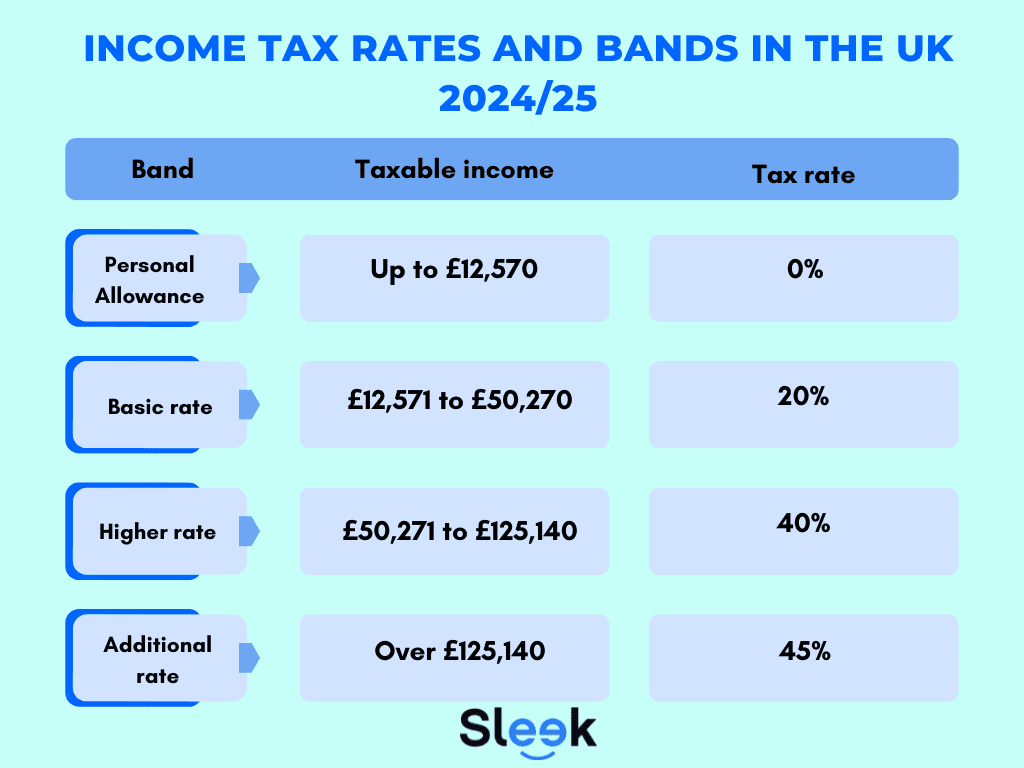

Personal allowance

For the 2024/25 tax year, the personal allowance is £12,570. This means you can earn up to this amount without paying a penny in income tax. It’s essentially your tax-free buffer.

Basic rate

Once your taxable income exceeds £12,570, you’ll start paying the basicstarting rate of 20% on earnings between £12,571 and £50,270. This tax band applies to the majority of taxpayers.

Higher rate

If your total income is over £50,270, you’ll pay the higher tax rate of 40% on anything you earn between £50,271 and £125,140. Around 4.2 million people in the UK fall into this bracket.

Additional rate

The highest earners, with a total income above £125,140, pay the additional rate of 45% on earnings over this amount. Less than 1% of the population are in this top income tax band.

How much tax will you pay based on your income?

Your income tax bill depends on how much of your salary falls within different UK tax brackets. Here’s a quick breakdown with an example.

Say your income tax is £55,000. The first £12,570 is tax-free thanks to your personal allowance. Then, you pay income tax at 20% on the next £37,700 (the portion between £12,571 and £50,270). Finally, the remaining £4,730 (from £50,271 to £55,000) is taxed at 40%.

If you do the math, your total income tax bill would be £9,422. Of course, these calculations can get tricky, which is why using an online tax calculator or consulting an accountant when filing your tax return can be a lifesaver.

What is the 60% tax rate in the UK and how can you avoid It?

There’s a quirky section of the UK tax brackets known as the 60% tax trap. It’s not an official tax band, but it can catch out unwary earners.

Here’s how it works: if your taxable income falls between £100,000 and £125,140, your tax-free personal allowance gets gradually taken away. For every £2 you earn over £100,000, you lose £1 of allowance.

In effect, until you start paying the additional 45% tax rate at £125,140, your marginal tax rate is a whopping 60%.

The good news is there are ways to sidestep this 60% effective rate. Making pension contributions or charitable donations can reduce your taxable income back below the £100,000 threshold, restoring your full personal allowance and tax reliefs.

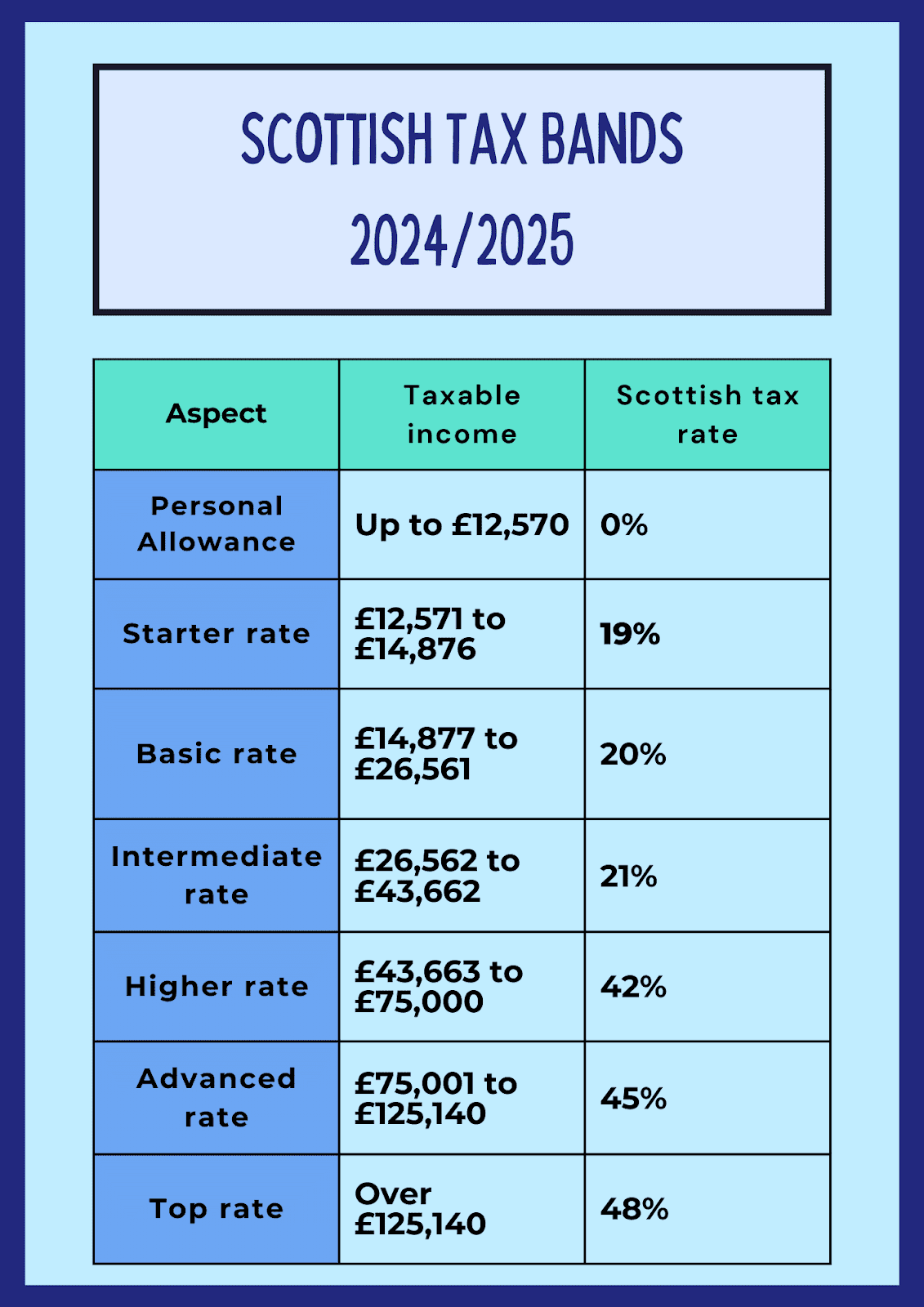

Understanding the Scottish Income Tax System

If you live in Scotland, you’ll face a slightly different set of income tax rates and bands than the rest of the UK. The Scottish system has five tax bands, ranging from a 19% starter rate to a 48% top rate.

For the 2024/25 tax year, the starter rate of 19% applies to Scottish income between £12,571 and £14,876. The basic rate of 20% then kicks in until £26,561.

There’s an intermediate rate of 21% for earnings between £25,689 and £43,662, then a higher rate of 45% up to £125,140. Finally, the top rate of the Scottish income tax of 48% applies to any Scottish income above £125,140.

How do the Welsh and Northern Irish tax bands differ?

Wales shares the same income tax bands and rates as England and Northern Ireland, with one key difference. Welsh taxpayers pay 10 percentage points of their income tax directly to the Welsh Government, which has the power to set its own rates.

So far, the Welsh Government has kept its rates in line with England and Northern Ireland, but it’s worth keeping an eye on in case this changes in future.

Key Takeaway:

Understand the UK tax brackets to budget better. The 2023/24 rates include a £12,570 personal allowance and three income bands: basic (20%), higher (40%), and additional rate (45%). Watch out for the 60% trap if earning between £100k-£125k; pension contributions or donations can help reduce this.

Which tax system applies to you?

The tax system that applies to you in the UK depends on where you live. If you’re in England or Northern Ireland, you’ll pay the UK tax brackets and rates. But if you call Scotland or Wales home, things work a bit differently.

In Scotland, they have their own income tax rates and bands. And in Wales, while the rates and bands match England and Northern Ireland, Welsh taxpayers pay 10 percentage points of their income tax directly to the Welsh Government. So it’s important to know which system you fall under.

Checking your tax code and settings

To make sure you’re paying the right amount of tax, it’s a good idea to check your tax code and settings. You can do this by logging into your online HMRC account. There, you’ll be able to see which tax system applies to you based on the address they have on file.

While you’re logged in, you can also manage your cookie settings. Accepting additional cookies can help HMRC improve government services and deliver more personalized content. But if you’d rather not, you can always change your cookie settings at any time.

How can you reduce your taxes if you’re in a higher tax bracket?

If you find yourself in the higher or additional rate tax brackets, there are a few ways you can legally reduce your tax bill. One of the most effective is to make pension contributions. When you pay into your pension, you get tax relief at your highest marginal rate. So if you’re a higher rate taxpayer, you’ll get 40% tax relief on your contributions.

Another option is to claim marriage allowance if you’re married or in a civil partnership. This lets you transfer £1,260 of your personal allowance to your partner, as long as they’re a basic rate taxpayer. This can reduce your tax bill by up to £252 a year.

Be mindful of the personal allowance reduction

One thing to watch out for if you’re a high earner is the personal allowance reduction. For every £2 you earn over £100,000, your personal allowance is reduced by £1. This means that once you hit an income of £125,140, your personal allowance is zero.

If you’re looking to save on taxes, consider donating to charity or investing in venture capital trusts. With some smart financial planning, you can reduce your tax bill and keep more money in your pocket.

What are the different types of taxable income?

When it comes to paying tax, not all income is created equal. In the UK, there are three main types of taxable income: non-savings income, savings income, and dividend income. Each is taxed in a different way and has its own set of allowances.

Non-savings income includes things like your wages, pensions, and rental income. This is taxed at the standard income tax rates, starting at 20% and rising to 45% for the highest earners.

Savings income is the interest you earn on bank accounts or other savings products. For the 2023/24 tax year, you can earn up to £5,000 in savings interest tax-free, depending on which tax band you’re in.

Dividend income and the dividend allowance

If you own shares in a company, you might receive dividends as a form of income. The first £1,000 of dividends is tax-free thanks to the dividend allowance. After that, basic rate taxpayers pay 8.75% on dividends, while higher rate taxpayers pay 33.75% and additional rate taxpayers pay 39.35%.

It’s important to note that dividends are taxed after your other income. So if your non-savings and savings income already pushes you into the higher rate band, your dividends will be taxed at the higher dividend rate.

Understanding National Insurance Contributions

In addition to income tax, most workers in the UK also have to pay National Insurance contributions (NICs). These go towards funding state benefits like the NHS, state pension, and unemployment support.

For employees, NICs are deducted automatically from your paycheck, along with income tax. For the 2023/24 tax year, you pay 12% on earnings between £12,570 and £50,270 per year, and 2% on anything above that.

If you’re self-employed, you pay slightly lower rates of National insurance contributions, but you’re responsible for calculating and paying them yourself through your Self-Assessment tax return.

Benefits of National Insurance Contributions

Sure, NICs can take a bite out of your paycheck. But remember, by paying into the system during your working years, you’re setting yourself up to claim benefits like a state pension when you need them.

Paying NICs also entitles you to certain benefits even while you’re working, such as Statutory Sick Pay and Statutory Maternity Pay. So while it may feel like an extra tax, NICs play a vital role in the UK’s social safety net.

How do capital gains affect your tax bracket?

When you sell assets like stocks, real estate, or collectibles for a profit, those profits are called capital gains. Unlike your regular income, these gains have their own tax rules and rates called capital gains tax.

For the 2023/24 tax year, the capital gains tax allowance is £6,000. This means you can make up to £6,000 in capital gains before you start paying tax. If you’re a basic rate taxpayer, you’ll pay tax at 10% on your gains (18% on property). Higher and additional rate taxpayers pay 20% (28% on property).

Capital gains and your tax band

While capital gains are taxed separately from income, they can still affect which tax band you’re in. This is because your capital gains are added to your taxable income to determine your tax bracket.

For example, let’s say your income earned in a year is £45,000 and make a £10,000 capital gain. Your total taxable income would be £55,000 (assuming you’ve used up your capital gains allowance). This would push you into the higher rate tax band, meaning you’d pay 20% on your capital gain instead of 10%.

So if you’re planning to sell assets that will result in a large capital gain, it’s worth considering how it will impact your overall tax situation. By timing your sales carefully or spreading them across multiple tax years, you might be able to minimize the amount of tax you pay.

Key Takeaway:

Check which tax system applies to you based on your address. Log into your HMRC account to confirm and manage settings.

If you’re in a higher tax bracket, consider pension contributions or marriage allowance claims to reduce taxes legally.

Remember, making charitable donations can help offset the personal allowance reduction if you earn over £100,000.

Conclusion

So there you have it, folks – the wild and wacky world of “uk tax brackets”. We’ve navigated the treacherous waters of personal allowances, basic rates, the not-so-taxing tax return, and the ever-elusive 60% tax trap. We’ve even dared to venture into the realms of Scotland, Wales, and Northern Ireland, where tax bands take on a life of their own.

But here’s the thing: understanding your tax bracket is more than just a numbers game. It’s about taking control of your financial situation, being aware and up to date with all tax-free allowances, higher rates of tax and when they apply, and income tax reliefs.

Get expert assistance from dependable tax and accounting experts on Sleek. Our friendly professionals will help you make your business tax compliant and boost your returns while ensuring compliance with prevailing laws and regulations for tax in the UK.

450,000

businesses worldwide.

from 4,100+ reviews.

satisfaction rate from

16,000 surveyed clients.