Understanding the 40% Tax Bracket: What You Need to Know

Earning a higher income is a great achievement, but it’s important to understand how it affects your tax situation. If you’ve recently entered the 40% tax bracket, you may be wondering what this means for your finances.

In simple terms, the 40% tax bracket means a portion of your income is now subject to a higher tax rate. This can have a significant impact on your take-home pay, so it’s crucial to be well-informed and prepared.

In this blog post, we’ll guide you through the 40% tax bracket, explaining how it works and what you can do to optimise your tax strategy. We’ll cover everything from tax allowances and deductions to investment options and pension contributions.

By the end of this post, you’ll have a clear understanding of how the 40% tax bracket affects you and what steps you can take to minimise your tax liability.

What is the 40% tax bracket?

In the UK, the 40% tax bracket refers to the “higher rate” of income tax. For the 2023-2024 tax year, this rate applies to income earned between £50,271 and £125,140.

It’s important to understand that the UK operates a marginal tax system, meaning you only pay the specified tax rate on the portion of your income that falls within that specific tax bracket.

Income tax rates for 2023/24 and 2024/25

Let’s take a closer look at the current income tax rates in the UK, as understanding these thresholds is key to grasping how the 40% tax bracket affects you:

Tax Year 2023/24 (England, Wales, and Northern Ireland):

Tax Band | Taxable Income | Rate |

Personal Allowance | Up to £12,570 | 0% |

Basic Rate | £12,571 to £50,270 | 20% |

Higher Rate | £50,271 to £125,140 | 40% |

Additional Rate | over £125,140 | 45% |

Tax Year 2024/25 (England, Wales, and Northern Ireland):

The tax rates and bands remain the same as in the 2023/24 tax year.

Scotland has slightly different income tax bands and rates. Be sure to check the specific rates for Scotland if you are a Scottish taxpayer.

How the 40% tax bracket works

If your total income for the tax year is £60,000, you would pay:

- 0% on the first £12,570 (your Personal Allowance)

- 20% on your earnings between £12,571 and £50,270

- 40% on your earnings between £50,271 and £60,000

As you can see, the 40% higher rate tax band kicks in once your income exceeds £50,270 (after taking into account your Personal Allowance). Any income you earn above this threshold will be taxed at 40% until you reach the additional rate threshold of £125,140.

What income is taxed at 40%

So, what exactly counts as taxable income? It includes your salary or wages, any profits you make from self-employment, dividend income, rental income, and even some state benefits. If you’re not sure what your taxable income is, you can use HMRC’s online calculator to get an estimate.

Don’t forget, you may qualify for tax reliefs or allowances that can lower your taxable income and help you avoid jumping into a higher tax bracket. We’ll dive into the details of these options in just a bit, so stay tuned.

If your taxable income is above £50,270, you’ll be shelling out 40% tax on every penny over that threshold.

How to determine if you’re in the 40% tax bracket

Now that you know what the 40% tax bracket is, you might be wondering how to figure out if you fall into that category. Don’t worry, it’s not as complicated as it sounds.

1) Calculating your taxable income

The first step is to calculate your taxable income. This is the total amount of income you receive in a tax year, minus any tax allowances or reliefs you’re entitled to.

For most people, the biggest tax allowance is the Personal Allowance. For the 2023/24 tax year, the standard Personal Allowance is £12,570. This means you can earn up to £12,570 without paying any income tax at all.

Not sure about the tax on freelancers? Fret not, we have created just the guide for you.

2) Understanding your tax code

Your tax code is another important factor in determining your tax bracket. It’s a series of numbers and letters that tells your employer or pension provider how much tax to deduct from your pay.

The most common tax code for the 2023/24 tax year is 1257L. This means you’re entitled to the standard Personal Allowance of £12,570. If your tax code is different, it might mean you have a higher or lower Personal Allowance, or that you’re receiving other tax reliefs.

3) Using HMRC’s income tax calculator

If you’re still not sure whether you’re in the 40% tax bracket, you can use HMRC’s online calculator. It’s a quick and easy way to estimate your income tax for the current tax year.

Just enter your expected income, tax code, and any other relevant information, and the calculator will do the rest. It’ll show you how much tax you’ll pay at each rate, including the 40% higher rate if applicable.

Remember, this is just an estimate based on the information you provide. Your actual tax bill might be different, especially if your circumstances change during the tax year.

Tax allowances and reliefs for higher rate taxpayers

Just because you’re in the 40% tax bracket doesn’t mean you have to pay that much tax on all your income. There are several tax allowances and reliefs available that can help reduce your tax bill.

Tax allowances and reliefs for higher rate taxpers in the 40% tax bracket

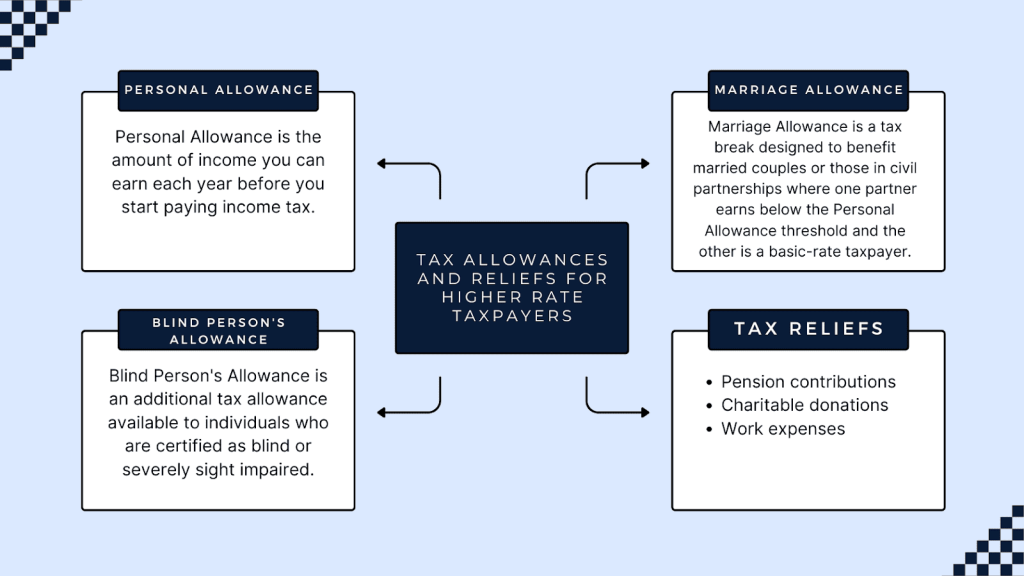

1) Personal allowance

The standard Personal Allowance for the 2023/24 tax year is £12,570. This means you can earn up to that amount without paying any income tax at all.

However, if your taxable income is over £100,000, your Personal Allowance starts to be reduced. For every £2 you earn over £100,000, your Personal Allowance goes down by £1. This means that if you earn £125,140 or more, you won’t get any Personal Allowance at all.

2) Blind person’s allowance

If you’re registered as blind or severely sight impaired, you might be entitled to the Blind Person’s Allowance. This is an extra tax-free allowance on top of your Personal Allowance.

For the 2023/24 tax year, the Blind Person’s Allowance is £2,870. This means you can earn an additional £2,870 before you start paying income tax.

3) Marriage allowance

If you’re married or in a civil partnership, you might be able to benefit from the Marriage Allowance. This allows you to transfer some of your unused Personal Allowance to your partner, as long as they’re a basic rate taxpayer.

Did you know that for the 2023/24 tax year, you can shift up to £1,260 of your Personal Allowance to your significant other? By doing so, you might be able to help them keep an extra £252 in their pocket come tax time.

Tax reliefs available

There are also several tax reliefs available that can reduce your taxable income and potentially keep you out of the higher tax bracket. Some common ones include:

- Pension contributions: You can get tax relief on money you pay into a pension, up to certain limits.

- Charitable donations: If you donate to a registered charity using Gift Aid, you can claim back the tax on your donation.

- Work expenses: If you have to pay for things like travel or equipment for your job, you might be able to claim tax relief on those expenses.

It’s worth taking some time to research which tax reliefs you might be eligible for. They can make a big difference to your overall tax bill.

Strategies to reduce your taxable income

If you’re looking for ways to reduce your taxable income and potentially avoid the 40% tax bracket, there are a few strategies you can try.

Making pension contributions

One of the most effective ways to reduce your taxable income is to make contributions to a pension. The money you pay into a pension is tax-free, up to certain limits.

For the 2023/24 tax year, you can contribute up to 100% of your earnings or £40,000 (whichever is lower) and still get tax relief. If you’re a higher rate taxpayer, this means you’ll get 40% tax relief on your contributions.

Charitable donations

Donating to charity can also help reduce your taxable income. If you donate through Gift Aid, the charity can claim back the basic rate tax on your donation. As a higher rate taxpayer, you can then claim back the difference between the basic rate and the higher rate on your tax return.

For example, if you donate £100 to charity through Gift Aid, the charity will receive £125 (£100 plus the basic rate tax of £25). You can then claim back the additional £25 (the difference between the basic rate and the higher rate) on your tax return.

Salary sacrifice schemes

Looking to boost your benefits package? Some companies provide salary sacrifice schemes that let you trade a portion of your paycheck for perks like childcare vouchers or cycle-to-work programs.

By contributing pre-tax dollars from your paycheck, you’re not only scoring valuable benefits but also shrinking your taxable income. That means you’ll owe less in taxes while still enjoying the perks of your benefits package.

Tax-efficient investments

Want to watch your wealth grow without the taxman taking a big bite? Consider investing in ISAs or pensions – they’re designed to be tax-efficient, so you keep more of what you earn.

With an ISA, you can save or invest up to £20,000 per year (as of 2023/24) without paying any tax on the interest or investment returns. And as we’ve seen, pension contributions can be a great way to reduce your taxable income while also saving for retirement.

Of course, investing always carries some risk, so it’s important to do your research and seek professional advice before making any big decisions.

How to claim tax relief as a higher rate taxpayer

If you’re a higher rate taxpayer and you think you might be eligible for some of the tax reliefs we’ve talked about, you’ll need to know how to claim them.

Claiming via self-assessment

If you’re required to file a self-assessment tax return (for example, if you’re self-employed or have rental income), you can claim most tax reliefs through the return.

When you fill out the return, you’ll be asked about any pension contributions, charitable donations, or work expenses you want to claim relief on. Make sure you keep good records throughout the year so you have all the information you need when it comes time to file.

Claiming marriage allowance

If you want to claim the Marriage Allowance, you can do it online through the gov.uk website. The partner with the lower income needs to apply, and they’ll need both partners’ National Insurance numbers.

If your application is successful, HMRC will adjust your tax codes so that the higher-earning partner gets the extra allowance. This will be reflected in their take-home pay.

Claiming work-related expenses

If you’ve been paying out of pocket for work-related expenses, you might be able to get some of that money back come tax time. Professional fees, travel costs, and tools or equipment needed for your job are all potentially eligible for tax relief if your employer hasn’t reimbursed you.

You can claim these expenses either through your self-assessment tax return or by filling out a P87 form and sending it to HMRC. Make sure you keep receipts or other proof of your expenses, as HMRC may ask to see them.

Claiming tax relief can seem like a bit of a hassle, but it’s worth doing if you think you’re eligible. Even small amounts can add up over time, and it’s always better to pay the right amount of tax rather than too much.

Key Takeaway:

Crack the 40% tax bracket by understanding it’s not all your income that gets taxed at this rate, just the bit over £50,270. Use HMRC’s calculator to see where you stand and explore reliefs like Pension Contributions or Charitable Donations to keep more of your money.

Conclusion

So, there you have it—the lowdown on the 40% tax bracket. It might seem daunting at first, but with a little bit of knowledge and some smart strategies, you can make it work for you.

Maximising your income means minimising your taxes. How? By understanding tax brackets and taking steps to reduce your taxable income. Contributing to a pension, donating to charity, and investing in tax-efficient vehicles are all smart moves. The more you know about how the system works, the more money you can keep for yourself and your family.

Conquer the 40% tax bracket by staying informed and taking decisive action. Keep a close eye on your money and make savvy financial moves. Do this, and you’ll navigate the bracket with ease, coming out victorious on the other side.

Sleek helps businesses by handling all of their accounting and tax matters.