What is Personal Tax Allowance in the UK and how can I claim it?

Personal Allowance is the amount of income you do not pay tax on. You are entitled to receive your Personal Allowance free of tax each year, and it is given to you automatically, rather than being something you need to claim.

Like most tax allowances in the UK, Personal Allowance works by reducing your taxable income. Let’s examine how the UK Personal Allowance works and its implications on your finances.

Personal Allowance: how much am I entitled to?

Employed people in the UK are entitled to an Income Tax Personal Allowance, even those only doing odd jobs or part-time work. This is the amount of money you’re entitled to earn without paying Income Tax on it.

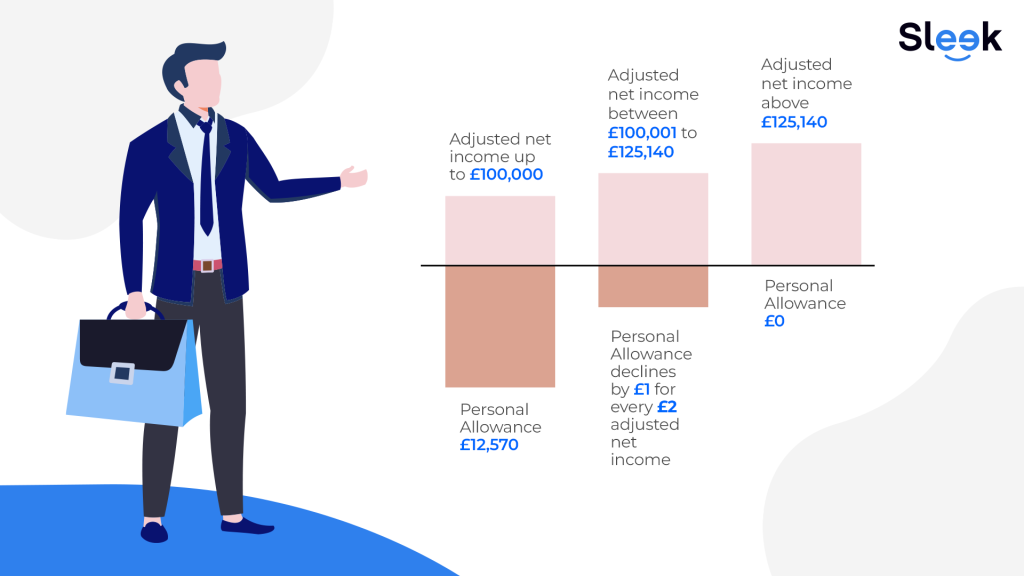

For the current year, your Personal Allowance is £12,570. Any income you earn after that will be taxable. Your Personal Allowance might be bigger if you claim a Marriage Allowance or a Blind Person’s Allowance, or it might be smaller if you’re a high earner.

Personal Allowance when your income is above £100,000

If you earn over £100,000, your Personal Allowance will go down by £1 for every £2 that your adjusted net income is above £100,000. This means your allowance will be zero if your income is £125,140 or above.

What is Income Tax?

Income Tax is a tax you pay on your income. You do not have to pay taxes on all types of income. Some income is tax-free.

- salary and some benefits from your job

- profits from your own business

- some government grants and support payments

- most pensions

- most rental income

- income from a trust

- savings interest (over your savings allowance)

- the first £1,000 of income from self-employment

- the first £1,000 of income from rental income (except under the Rent a Room Scheme)

- income from Individual Savings Accounts (ISAs) and National Savings Certificates

- dividends from company shares

- some state benefits

- premium bond or National Lottery wins

How much Income Tax will I pay?

As your income increases, so does the amount of Income Tax you pay. But you don’t pay tax at the same income tax rates on all your income. Instead, Income Tax is made up of different income tax bands. In order to find out how much Income Tax you will pay, you will need to determine your taxable income (your income above your Personal Allowance) and then how much of your income falls within each tax band.

The three Income Tax bands

The UK has 3 tax bands with rates of 20%, 40%, and 45%.

If you have a standard Personal Allowance, the table below shows the tax rates for Income Tax for each band.

Band | Taxable income | Tax rate |

Personal Allowance | Up to £12,570 | 0% |

Basic rate | £12,571 to £50,270 | 20% |

Higher rate | £50,271 to £125,140 | 40% |

Additional rate | Over £125,140 | 45% |

If you are a PAYE taxpayer in the UK, you can easily calculate your income tax here.

Self-employed taxes: How do they work?

Do you run your business as a sole trader or a limited company?

As a sole trader, in the eyes of the law, you and your business are viewed as the same entity. Your combined business revenues and other income will be taxed at the same rate as any other individual. You will be able to deduct permissible business expenses from your profits to arrive at your net taxable business profits.

You’ll also need to register with HMRC (HM Revenue and Customs), file a Self Assessment tax return, and maintain all records, unlike an employee where the employer deducts taxes from the paycheck and takes care of all paperwork.

But if you run a limited company, as a director you are an employee in the company and tax will be taken from your paycheck. If you also receive dividends, you will need to file your Self Assessment return as well. And of course, your company will have to pay Corporation Tax.

Other tax-free allowances

Your Personal Allowance works differently if you receive other tax-free allowances such as Marriage Allowance, starting rate for savings, Personal Savings Allowance, Dividend Allowance, or Trading Allowance.

Marriage Allowance: If you are a married couple or partner in a civil partnership, the one of you earns an income lower than their Personal Allowance, that person can transfer £1,260 of their Personal Allowance to their partner. But if both of you earn more than the UK Personal Allowance, then you will not be entitled to this.

Blind Person’s Allowance: If you are blind or severely sight impaired, you can claim for your Personal Allowance to be increased by £2,870. You can also transfer this allowance to your spouse or civil partner if you earn less than your Personal Allowance.

Starting rate for savings: If your income is lower than £17,570, you are also entitled to pay 0% tax on any savings interest earned up to £5,000. This decreases with your income. For example, you will only be entitled to the full £5,000 interest savings if you earn £12,570 or less. Above £12,570, for every £1 extra you earn your starting rate for savings will also be reduced by £1. Of course, there are also other ways to earn tax-free savings, such as with an Individual Savings Account (ISA).

Personal Savings Allowance: This allowance can be used on top of your starting rate for savings. This allowance allows you to receive up to £1,000 of tax-free interest, depending on which Income Tax you fall into:

Income Tax Band | Allowance |

Basic rate (for income up to £37,700) | £1,000 |

Higher rate (for income between £37,701 and £125,140) | £500 |

Additional rate (for income over £125,141) | £0 |

The Personal Savings Allowance covers various kinds of interest, from bank account savings and trust funds to government/company bonds and most types of life annuity payments.

Trading allowance: If you are self-employed, you will get a trading allowance that makes the first £1000 you earn tax-free.

Dividend allowance: If you own shares in a company, you will be entitled to a dividend allowance each year. For the tax year 2023/24, the dividend allowance is £1,000. Any income earned from dividends above £1,000 will be taxed at 8.75% (Basic rate), 33.75% (Higher rate) and 39.35% (Additional rate).

Other UK tax relief schemes

The amount of Income Tax you pay can also be reduced if you qualify for any of the UK government’s tax relief schemes. You may be able to claim tax relief on certain business expenses or if you donate to a charity. If you make Maintenance Payments to an ex-spouse or civil partner, you can get tax relief of 10%, to a maximum of £401 a year.

National Insurance Contributions

Income Tax is not the only tax you will have to pay. You will also need to pay National Insurance. National Insurance Contributions (NIC) help to pay for state benefits like unemployment, retirement, or bereavement.

Most people who work in the UK have to pay NIC. You start paying NIC from the age of 16, once your earned income reaches a certain level.

There is no Personal Tax Allowance when it comes to NIC, nor is NIC deductible from taxable income, for either the employed or self-employed.

The amount of National Insurance you pay will depend on your employment status and how much you earn. In the tax year 2023/24, you will pay at the following rate:

As an employee, Class 1 National Insurance:

Earnings | Rate |

£242 to £967 a week | 12% |

Over £967 a week | 2% |

As self-employed Class 2 and Class 4 National Insurance for profits above £12,570:

Class 2 | £3.45 a week |

Class 4 | 9% on profits between £12,570 and £50,270 2% on profits over £50,270 |

What tax rates apply to me?

We understand if all of the above information, such as the various allowances and types of tax, is hard to navigate. So let us simplify it for you through an example.

In the tax year 2023/2024, Mary, who is employed, earns £29,570 in wages, £5,000 in savings interest, and £3,000 in dividends. Her total income is £37,570. What taxes will she pay?

As her taxable income exceeds £17,570, she is not entitled to the starting rate of savings. However, she is entitled to a Personal Savings Allowance of £1,000, as her income falls within the Basic rate.

Additionally, her dividend allowance will entitle her to £1,000 in tax-free dividend earnings.

After taking off her Personal Tax Allowance of £12,570 and her Personal Savings Allowance of £1,000, her taxable income is £23,000, which falls under the ‘basic rate’ tax band. Her taxes will be:

- 20% tax on £21,000 (wages and savings) = £4,200

- 8.75% tax on £2,000 (dividends) = £175

- Mary’s total Income Tax to be paid = £4,375

Personal Tax Allowance: in conclusion

Managing your income tax, contributions, and deductions can be a daunting task. Very often, you may have income that’s not from your employer or business, for example through savings or dividends.

Hiring a professional accountant can simplify things for you. Sleek can create your income tax returns and submit them online directly to HMRC. We can also help you save money on your accounting and ensure you never miss a deadline. If you’d like to speak to one of our advisors, please don’t hesitate to contact us now.

FAQs

As per UK Income tax laws, all non-savings and non-dividend income (that includes self-employed income, wages, pension, and rental income) is subject to your Personal Tax Allowance.

You can work this out by adding up your income from wages and savings in order to determine your tax band. This tax band will, in turn, dictate the percentage by which your dividends will be taxed.

Most tax allowances, like the Personal Tax Allowance, are deducted from your taxable income before tax is worked out. Others, such as Marriage Allowance, are given as a reduction in your tax bill. Some tax allowances will only be worked out by HMRC once you have submitted your Self Assessment tax return (if applicable).