How Can I Minimize My Corporation Tax Liability?

Running a business in the UK is no small feat, and tax season can feel like an added challenge. But what if you could lessen the financial burden? If you’ve ever asked yourself, “How can I minimize my corporation tax liability?”, you’re in the right place. Understanding and implementing effective tax strategies can significantly impact your bottom line, and we’re here to guide you.

In this blog post, we’ll share nine proven tips to help you answer the question, “How can I minimize my corporation tax liability?”. From leveraging tax reliefs to optimising your business structure, we’ll uncover practical strategies business owners can implement today to keep more of their hard-earned profits. So, let’s explore these tax-saving opportunities together.

Tip #1: Claim tax relief on business expenses

As a seasoned business owner, it is important to understand the value of claiming tax relief on all allowable business expenses. It’s not just about saving money; it’s about ensuring your company’s financial health and sustainability.

Understanding allowable business expenses

Here’s the deal: not every expense you incur is tax-deductible. To claim tax relief, your expenses must be wholly and exclusively for business purposes. This includes things like office rent, equipment, travel costs, and employee salaries. HMRC provides detailed guidance on what qualifies as an allowable business expense. It’s crucial to familiarise yourself with these rules to maximise your tax savings.

Keeping accurate records

Keeping meticulous records is the key to claiming all the tax relief you’re entitled to. Trust us, many have learned this lesson the hard way. Every time you incur a business expense, keep the receipt or invoice. Use accounting software to track your expenses throughout the year. This will make your life so much easier when it’s time to file your tax return.

Maximising tax relief on business expenses

Here’s a pro tip: don’t just settle for claiming the obvious expenses. Dig deeper and look for every legitimate expense you can claim. For example, if you work from home, you may be able to claim a portion of your utility bills and rent as a business expense. If you use your personal car for business travel, keep a mileage log and claim the appropriate tax relief. Consider working with a tax specialist to identify any often-overlooked business expenses you could be claiming. A professional eye can help you uncover significant tax savings.

Tip #2: Utilise capital allowances

Capital allowances are a game-changer when it comes to reducing your corporation tax bill. If you’re not taking full advantage of this tax relief, you’re leaving money on the table.

Understanding capital allowances

In a nutshell, capital allowances let you claim tax relief on the cost of assets you buy for your business. This includes things like machinery, equipment, and vehicles. The type of asset determines how much tax relief you can claim and over what period. It’s a bit complex, but well worth getting your head around.

Annual investment allowance

The Annual Investment Allowance (AIA) is a real boon for businesses. It allows you to claim 100% tax relief on qualifying assets, up to a certain limit, in the year you buy them. For the 2023/24 tax year, the AIA limit is a whopping £1 million. This means you can potentially write off the full cost of significant investments against your taxable profits.

Writing down allowances

For assets that don’t qualify for the AIA or exceed the annual limit, you can still claim tax relief through writing down allowances. These allowances let you deduct a percentage of the asset’s cost from your taxable profits each year. The percentage depends on the type of asset, but it’s typically 18% or 6% per year. It’s not as immediate as the AIA, but it still provides valuable tax savings over the life of the business assets.

Tip #3: Make pension contributions through your company

One of the smartest ways to reduce your corporation tax bill is by making pension contributions through your company. It’s a win-win: you save for your future while reducing your tax liability today.

Tax benefits of company pension contributions

When your company makes a pension contribution on your behalf, it counts as an allowable business expense. This means it reduces your company’s taxable profits, which in turn lowers your corporation tax bill. But here’s the kicker: pension contributions are also tax-free for the recipient. So, you’re essentially getting a double tax benefit.

In need of a corporation tax guide? Check out a guide we have created just for you.

Choosing the right pension scheme

There are several types of company pension schemes, each with its own rules and tax implications. It’s crucial to choose the one that best aligns with your business goals and personal circumstances. For example, a defined contribution scheme allows you to set your own contribution levels, while a defined benefit scheme provides a guaranteed income in retirement. Consider factors like fees, investment options, and flexibility when selecting a pension provider. It’s worth getting professional advice to ensure you make the right choice.

Maximising pension contributions

As a company director, you can make significant pension contributions to reduce your corporation tax bill. The key is to stay within the annual and lifetime allowances set by HMRC. For the 2024/25 tax year, the annual allowance is £60,000, and the £1,073,100 lump sum allowance together with death benefit, replaced the lifetime allowance on April 6, 2024. By maximizing your contributions up to these limits, you can substantially reduce your tax liability while securing your financial future.

Stashing cash in your pension pot can help you live the life you want when you’re ready to ditch the 9-to-5. If you’re the boss of your own limited company, you can funnel employer contributions straight from your company account into your pension. The taxman usually sees these contributions as a business expense, so you won’t have to pay corporation tax on them.

— Hargreaves Lansdown (@HLInvest) March 5, 2023

Tip #4: Take advantage of the Patent Box Scheme

If your company holds patents, the Patent Box scheme can significantly reduce your corporation tax rate on profits derived from those patents. It’s a fantastic way to reward innovation and boost your bottom line.

Understanding the Patent Box Scheme

The Patent Box allows companies to apply a lower corporation tax rate of 10% to profits earned from patented inventions and certain other innovations. This is a substantial reduction from the standard 19% rate. To qualify, your company must own or exclusively license-in the patent and must have undertaken qualifying development on the patented invention. It’s a bit technical, but well worth exploring if you have patented inventions.

Qualifying for the Patent Box

Not all patents are eligible for the Patent Box. To qualify, the patent must have been granted by the UK Intellectual Property Office, the European Patent Office, or certain other specified EEA countries. Additionally, your company must have made a significant contribution to the creation or development of the patented invention. You can’t simply acquire a patent and claim the tax relief. It’s important to keep detailed records of your research and development activities to support your Patent Box claim.

Calculating Patent Box relief

Calculating the actual tax relief under the Patent Box can be complex. It involves apportioning your company’s profits between those attributable to the patented invention and those that aren’t. There’s a formula for this, which takes into account factors like the percentage of your turnover derived from the patent and any routine returns or marketing assets. Given the complexity, it’s advisable to seek professional help when preparing a Patent Box claim. A qualified tax advisor can ensure you claim the maximum relief you’re entitled to.

Key Takeaway:

Slash your corporation tax bill by claiming all allowable business expenses, from office costs to employee salaries. Keep every receipt and track expenses with software for easy filing. Don’t miss out on capital allowances and pension contributions that can majorly cut taxes. And if you’ve got patents, the Patent Box scheme could lower your rate even more.

Tip #5: Implement an employee share scheme

Want to attract and retain top talent while also reducing your corporation tax bill? Implementing an employee share scheme could be the answer.

Types of employee share schemes

There are several types of share schemes to choose from, each with its own tax implications. Some popular options include Enterprise Management Incentives (EMI), Company Share Option Plans (CSOP), and Share Incentive Plans (SIP). The key is finding the scheme that aligns with your company’s goals and offers the most tax benefits. For some of our clients, EMI schemes worked well for SMEs looking to incentivize key employees.

Tax benefits of employee share schemes

Implementing an employee share scheme can provide tax advantages for both the company and its employees. Depending on the scheme, your company may be able to claim Corporation Tax relief on the costs associated with setting up and operating the scheme. And employees can potentially benefit from reduced Income Tax and National Insurance contributions on their shares. It’s a win-win situation that can help you attract and retain the best talent while also minimising your tax liabilities.

Not sure what the corporation tax for small businesses are? Fret not, we have created an article that explains all you need to know.

Setting up an employee share scheme

While the tax benefits are appealing, setting up an employee share scheme is no simple feat. There are various legal and tax considerations to navigate. Our advice? Seek professional guidance from a qualified accountant or tax specialist, like us here at Sleek. We can help ensure your scheme is structured correctly and complies with all relevant regulations. Trust us, getting expert advice upfront can save you a lot of headaches down the road. It’s an investment in your company’s future success.

Tip #6: Claim marginal relief

If your company’s profits fall within a certain range, you may be able to claim marginal relief and reduce your corporation tax bill. Here’s what you need to know.

Understanding marginal relief

Marginal relief is a tax relief available to companies with profits between £50,000 and £250,000. It aims to ease the transition from the small profits rate (19%) to the main Corporation Tax rate (25% as of April 2023). Think of it as a gradual increase in your effective tax rate, rather than a sudden jump. This relief can make a significant difference in your company’s tax liabilities.

Qualifying for marginal relief

To qualify for marginal relief, your company’s profits must fall within the marginal relief limits, which are £50,000 to £250,000 for the 2023/24 tax year. Keep in mind that these limits are proportionately reduced for accounting periods of less than 12 months. So, if your company’s accounting period is shorter, you’ll need to adjust your calculations accordingly.

Calculating marginal relief

Calculating marginal relief can be a bit tricky. It involves using a complex formula that takes into account your company’s profits and the upper and lower limits of the marginal relief band. The relief is applied as a reduction to your Corporation Tax liability. To ensure you’re claiming the correct amount, we recommend using HMRC’s marginal relief calculator or consulting with a tax professional. Getting these calculations right can make a big difference in your company’s bottom line. It’s worth taking the time to understand how marginal relief works and how it can benefit your business.

Tip #7: Consider setting up a holding company structure

If you’re looking for ways to optimise your company’s tax position, setting up a holding company structure could be a smart move. Let’s explore the benefits and implications.

Benefits of a Holding Company Structure

A holding company structure can offer various tax benefits. For one, it allows you to offset losses from one subsidiary against profits from another, thereby reducing your overall Corporation Tax liability. It can also facilitate the transfer of assets between group companies without triggering tax charges. This flexibility can be invaluable as your business grows and evolves.

Setting Up a Holding Company

To set up a holding company structure, you’ll need to incorporate a new company that will own shares in your existing trading company (or companies). The holding company can be a pure holding company with no trading activities of its own, or it can be a mixed holding and trading company. The choice depends on your specific business needs and goals.

Tax Implications of a Holding Company Structure

While a holding company structure can provide tax benefits, it’s important to consider the potential drawbacks and complexities. These may include increased administrative costs, additional compliance requirements, and the need to navigate complex group tax rules. It’s not a decision to be made lightly. As with any major business restructuring, we strongly recommend seeking professional advice before setting up a holding company.

Tip #8: Seek professional advice

Corporation tax can be overwhelming, especially as your business grows. That’s where professional advice from a tax specialist comes in.

Choosing the right tax specialist

When selecting a tax specialist, look for someone who understands your industry and business structure. They should be up-to-date with the latest tax regulations and able to provide tailored advice to help you minimise your Corporation Tax liability. Not all tax specialists are created equal. Take the time to find someone who is qualified, experienced, and truly understands your business needs.

Maximising tax efficiency with professional advice

Hiring a skilled tax specialist or tapping an accounting and tax services like us here at Sleek can help you identify opportunities to maximise your tax efficiency that you may have overlooked. They can guide you through complex areas like employee share schemes, holding company structures, and marginal relief. The right professional advice can be a game-changer when it comes to minimising your corporation tax liabilities. It’s an investment in your company’s financial health and future success.

Staying up-to-date with tax regulations

Tax regulations are constantly evolving, and it can be challenging to stay on top of the latest changes. That’s where having a trusted tax specialist on your side can make all the difference. They can help you go through tax and ensure you remain compliant while minimising your liabilities. It’s about staying proactive rather than reactive when it comes to managing your corporation tax affairs. Seeking professional advice is not an expense; it’s an investment. The right guidance can save you money, time, and stress in the long run. So don’t hesitate to reach out to a qualified tax specialist to help you optimise your company’s tax position.

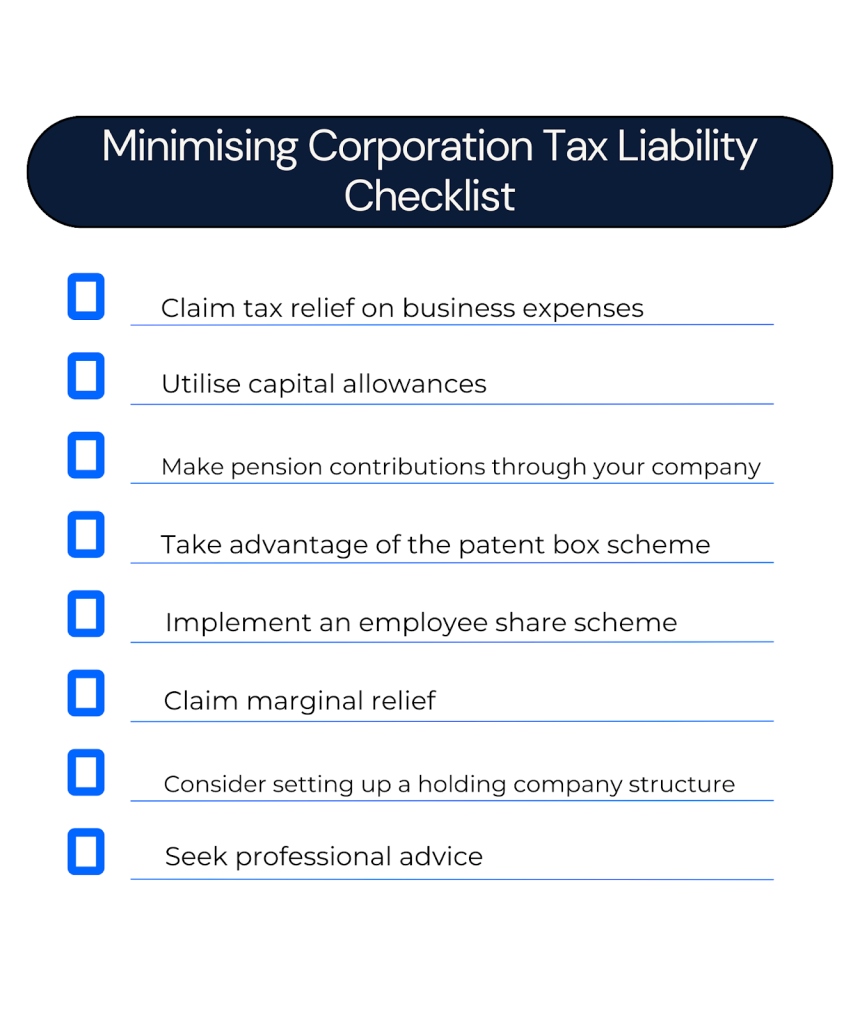

Minimising Corporation Tax Liability Checklist

Key Takeaway:

Slash your corporation tax bill by implementing an employee share scheme, exploring marginal relief, and maybe setting up a holding company. Don’t forget to get savvy advice from a top-notch tax specialist.

Conclusion

Now that your question: How can I minimize my corporation tax liability has been answered, you’ll realize that it doesn’t have to be a headache. By claiming all your allowable expenses, utilising capital allowances, making pension contributions, taking advantage of the Patent Box scheme, implementing an employee share scheme, claiming marginal relief, considering a holding company structure, and seeking professional advice, you can legally reduce your tax bill and keep more of your profits.

No two businesses are alike, so it’s crucial to find the corporation tax strategies that fit your company like a glove. If you’re feeling lost in the labyrinth of tax laws, don’t hesitate to call in reinforcements – a savvy tax specialist can be your trusty guide through the twists and turns.

So go ahead, put these strategies into action, and start enjoying the benefits of a lower corporation tax liability today. Your business (and your bank account) will thank you.

FAQs in Relation to How Can I Minimize My Corporation Tax Liability?

What lowers corporation tax?

Claiming allowable business expenses, using capital allowances for assets, and making company pension contributions can all lower your corporation tax.

What reduces tax liability the most?

Making the most of schemes like Patent Box for patented inventions or implementing an employee share scheme often slashes tax liabilities significantly.

Can I buy property to reduce corporation tax?

Yes, buying property through your limited company allows you to claim capital allowances, reducing overall corporation tax.

What is the most tax efficient way to pay yourself as a director?

Paying a small salary up to the National Insurance threshold combined with dividends from profits ensures maximum efficiency in reducing personal and corporate taxes.