Corporation tax is something every UK-based limited company must grapple with. But understanding how this tax impacts your business and the available options for potential reduction doesn’t have to feel overwhelming. This article aims to demystify this important financial obligation.

With the right knowledge, you can turn corporation tax into a source of strategic savings for your start-up. The UK offers tax reliefs and allowances, like the Annual Investment Allowance and R&D tax relief, tailored to help small businesses thrive.

In this guide, we’ll walk you through the essentials of managing corporation tax efficiently and share practical tips to boost your start-up’s financial health. Ready to make corporation tax work for you? Let’s get started.

What exactly is corporation tax?

At its core, corporation tax is a tax levied by HM Revenue and Customs (HMRC) on the annual taxable profits of UK-based companies. This tax applies to profits earned from various avenues like:

- Regular business activities.

- Investment ventures.

- Selling assets (such as property or shares) for more than their original cost.

Unlike individuals, companies don’t enjoy a tax-free allowance; hence, all company profits are considered taxable.

Who needs to pay corporation tax?

Corporation tax applies to limited companies in the UK. But, other organisations might find themselves liable even without being formally incorporated. This includes entities like:

- Housing associations.

- Membership-based organisations like clubs and societies.

- Co-operatives.

Sole traders and partnerships don’t have to deal with corporation tax. Instead, their earnings fall under the self-assessment income tax system.

How is corporation tax calculated?

Now that we know who pays corporation tax, let’s understand how this tax is calculated. It all boils down to a company’s ‘corporation tax accounting period’. This period typically aligns with a company’s financial year. Let’s look at the current corporation tax rates for 2023-24 in the UK:

Profit Level | Corporation Tax Rate

|

|---|---|

Above £250,000 | 25% (main rate) |

Below £50,000 | 19% (small profits rate) |

Between £50,000 and £250,000 | Sliding rate (marginal relief applies) |

Those whose profit falls between the lower and upper limits may benefit from marginal relief. You can use the provided marginal relief corporation tax calculator by the government for a more precise calculation.

It’s also important to note that certain industries might have specific corporation tax rules. Take, for instance, the oil and gas sector, this industry follows a distinct tax regime for offshore operations. This just goes to show that while we aim to be comprehensive, staying updated on industry-specific regulations is always crucial.

Remember, your responsibility as a director includes ensuring accurate calculations, timely filing of the company tax return (CT600), and, of course, paying the bill on time. Don’t let the details bog you down; this is where a qualified accountant can prove invaluable.

Their expertise can ensure you benefit from every allowable deduction and capital allowances, minimising your tax obligations without a hitch.

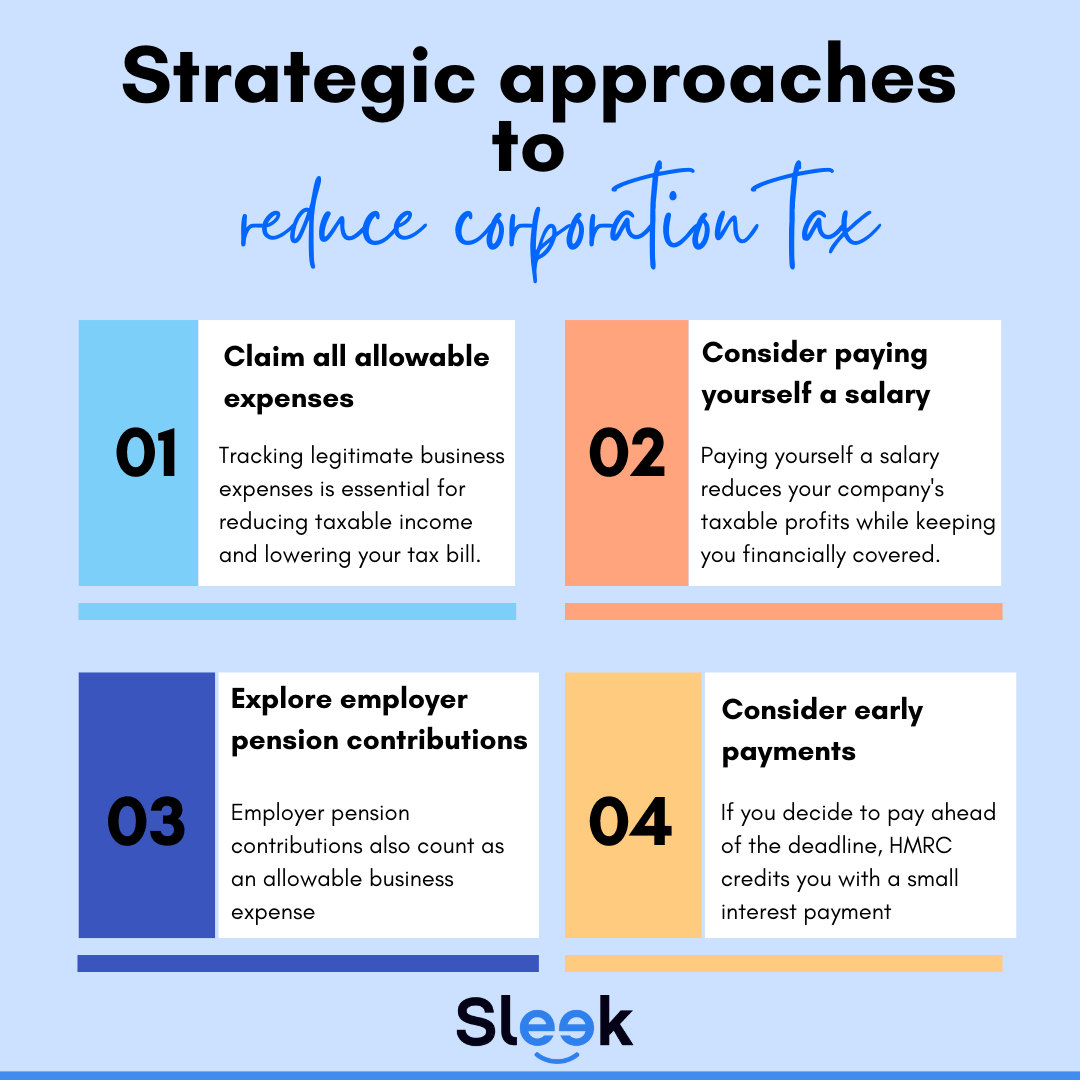

Strategic approaches to reduce corporation tax

Minimising your tax liabilities within legal boundaries is savvy business practice. Let’s dive into some strategies to potentially reduce your corporation tax:

1. Claim all allowable expenses

Keeping track of legitimate business expenses is non-negotiable. This meticulous record-keeping lets you deduct these costs from your profit, lowering your taxable income and leading to a smaller tax bill.

Documentation is key. HMRC could deny your claim if your records lack clarity. For example, keeping all receipts for items purchased that relate to your business, such as contractor insurance, can help support your business expense claims.

2. Consider paying yourself a salary

Though you may be the driving force behind your limited company, legally, you and your company are distinct entities. You can choose to draw a salary. Like with other employees, your salary (along with employer National Insurance contributions) is deductible from the company’s profits before tax.

However, remember that you will need to pay income tax on your salary and make employee National Insurance contributions. Therefore, it may be worth keeping your salary under the higher rate income tax threshold to optimise your tax liability.

3. Explore employer pension contributions

Have you thought about making employer pension contributions? They aren’t just a smart retirement move; they also count as an allowable business expense. This means they’re deducted before your corporation tax is calculated, shrinking that bill further.

There are annual limits to contributions. Research this or speak with a financial advisor for specifics relevant to your situation. Understanding things like the annual allowance and navigating the complexities of pensions can make a real difference.

4. Consider early payments

Being ahead of your corporation tax obligations could mean slight financial gains. If you decide to pay ahead of the deadline, HMRC credits you with a small interest payment, usually 0.5%.

However, the corporation tax timing matters. They typically calculate interest starting from six months and 13 days after your accounting period begins, up until your actual payment date.

When are corporation tax payments due?

Knowing when to pay is just as crucial as knowing how much to pay. Missing these deadlines invites unnecessary financial penalties. Corporation tax, unlike other UK taxes, is generally paid before you actually file your company tax return. Typically, you need to make this payment nine months and one day after the end of your company’s accounting period.

Let’s illustrate this with a scenario. Imagine your accounting period ends on 31 March. This makes your corporation tax payment due by 1 January of the following year. This differs from the tax return, which you must file within three months of this payment date.

Larger businesses with profits over £1.5m operate differently. These companies make payments in installments throughout the year.

Understanding penalties and surcharges

Missing deadlines can have consequences. Late tax payments or inaccurate submissions could lead to penalties or interest on outstanding balances. HMRC wields the authority to deploy various enforcement measures to recover unpaid sums. These range from utilising debt collection agencies or initiating court proceedings, to potentially even making you bankrupt.

Open communication with HMRC is key in challenging times. If meeting your tax obligations becomes difficult, connect with them immediately. There are options like “Time to Pay” arrangements that allow you to spread out payments with a plan.

However, remember that HMRC might require detailed justification and a clear strategy for full repayment, possibly involving asset liquidation, before considering such an arrangement. Public bodies often provide resources for businesses struggling with tax obligations.

Reliable professional services for your business:

At Sleek, we provide cost-efficient and hassle-free accounting, tax, business registration services, and more. With over 450,000 entrepreneurs like you successfully assisted, our expertise ensures your limited company is set up correctly and complies with all tax and legal requirements.

Trust Sleek to simplify your corporation tax, so you can focus on growing your business. Share your enquiry now and our professional team will understand your unique requirements and assist you accordingly.

Our commitment to excellence is reflected in our ratings, boasting a 4.9 on Google and a 4.8 on Trustpilot.

Final thoughts

Corporation tax is undeniably an important part of running a limited company in the UK. But, with the right information and planning, managing this obligation needn’t be an uphill battle.

Remember that utilising available tools like online resources, tax calculators, and professional guidance from accountants, empowers informed decisions and more efficient tax management. This leaves you to channel your energy into what you do best – steering your business toward success.

Conclusion

Navigating corporation tax is a crucial skill for every UK entrepreneur. Staying informed, engaging with available resources, and potentially collaborating with a qualified accountant can transform this complex duty into a manageable facet of running a profitable, sustainable enterprise.

Taking a proactive stance to understand and manage corporation tax is paramount to achieving both financial success and peace of mind. Regularly reviewing your business insurance needs, including aspects like contractor insurance, can also contribute to a more financially secure business.

Additionally, keeping an eye on relevant government activity is essential for staying compliant with evolving tax policies. Changes in corporation tax rates or relief schemes can directly affect your limited company’s financial health. The UK government often updates its guidance, making the official navigation menu of HMRC’s website a valuable resource to track these changes and plan accordingly.

As the owner of a limited company, accessing local services like business advisory programs or community-led financial workshops can provide personalized support. These resources not only help you manage your corporation tax responsibilities more efficiently but can also offer tailored advice that might unlock new avenues for savings and growth.