Running a limited company means juggling financial priorities, and planning for retirement should be high on that list. A company director pension isn’t just a safeguard for the future; it’s also a smart way to save on taxes today. With strategic pension contributions, you can boost your retirement fund while potentially benefiting from generous tax relief.

Understanding how a company director pension works, especially in relation to tax relief, can unlock significant savings for your business and personal finances. Contributions made by your company aren’t subject to income tax or National Insurance, offering a direct route to maximising retirement savings.

In this guide, we’ll explore pension contributions strategy, tax relief opportunities, and how company directors can optimise their pensions. Discover how small adjustments in your pension contributions now can make a big difference in the years to come.

Understanding company director pensions

As a limited company director, a company director pension helps you save for retirement and potentially lower your tax burden. You’re not automatically enrolled in a workplace pension like employees.

It’s your responsibility to set one up and begin making pension contributions. A company director pension is a crucial element of retirement planning for limited companies.

Types of pension schemes

You can choose from several pension schemes: a Self-Invested Personal Pension (SIPP), stakeholder pension, or other private pensions.

A SIPP offers investment flexibility but requires careful management. Stakeholder pensions, along with other types of personal pensions, provide simplified investment strategies. You should research the pros and cons of each pension scheme type to determine the best one for your situation.

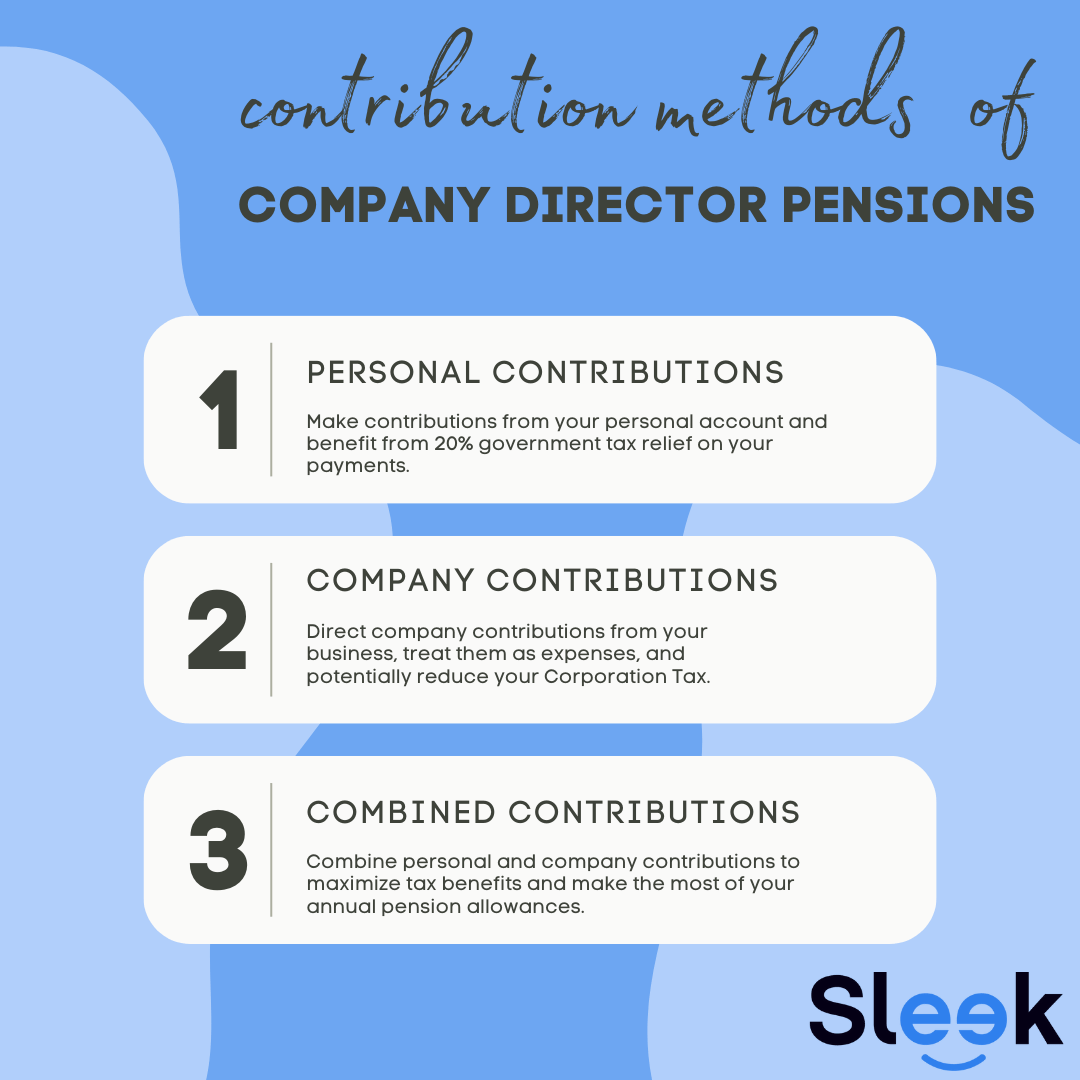

Contribution methods

Company director pensions offer various contribution methods, such as using a company pension or making personal contributions:

- Personal contributions: Pay in from your personal account, potentially funded through your salary (through PAYE), and receive 20% tax relief from the government. This is just one of many pension contribution strategies.

- Company contributions: These employer contributions, paid directly from your business, are treated as a business expense, potentially reducing your Corporation Tax (BIM46030 and BIM46035). Company contributions are part of tax planning but still count toward your annual pension allowance.

- Combined contributions: Combining personal and company contributions offers the benefits of both, each impacting your total allowances differently.

Navigating contribution limits and tax relief

Tax efficiency is a key benefit of company director pensions. However, understanding the limits and allowances can be complex. Proper retirement planning necessitates careful consideration of pension tax relief and how it applies to different contribution methods.

Annual allowance

The annual allowance is £60,000 (2024/25). This is the maximum you can contribute in a tax year while receiving full pension tax relief. This applies to company contributions, personal contributions (even from age 55), or a combination.

Tax relief reduces the “cost” of your contributions. The relief depends on your income tax band. Higher earners could get an additional 20-25% on top of the basic rate taxpayer’s 20%.

Carry forward

If you haven’t maximised your contributions in previous tax years, consider ‘carry forward’.

This rule lets you use unused allowance from the past three tax years, useful for larger lump sum contributions to offset high-income periods. Understanding the ‘carry forward’ rule can be useful for maximizing your company pension contributions.

Lump sum allowance

Typically, you can withdraw 25% of your pension pot tax-free. The individual lump sum allowance is £268,275.

Specific cases (serious illness, lump-sum death benefits) have a higher allowance of £1,073,100. Withdrawals exceeding these limits are taxed as income.

High-earning directors and the tapered annual allowance

Directors with high incomes (above £260,000 and total income including benefits over a second threshold) face different rules.

Your allowance might decrease, potentially to a minimum of £10,000. This is due to the tapered annual allowance, which reduces the allowance by £2 for every £1 earned over a threshold.

Affordable and reliable professional services for your business

At Sleek, we provide cost-efficient and hassle-free company formation services including accounting & tax services, tailored to your needs. Customers are fully supported by a UK-based team who are available on the phone or by email, and offer friendly, expert guidance throughout.

With over 450,000 SMEs successfully assisted, our expertise ensures your limited company is set up correctly and complies with all legal requirements.

Our commitment to excellence is reflected in our customer ratings – a 4.9 on Google and a 4.8 on Trustpilot.

Conclusion

A company director pension empowers you to take control of your retirement planning with flexibility in pension contributions. Whether you contribute personally or through employer pension contributions, each approach has unique tax advantages. By directing contributions through your company, for example, you can benefit from tax relief on qualifying contributions, reducing your corporate tax bill and adding value to your retirement fund.

Being strategic with pension contributions allows you to balance current cash flow with long-term savings. Every tax year offers new opportunities for tax relief, and staying informed about government guidelines can help you make the most of these benefits. This tailored approach ensures that your company director pension aligns with both your business needs and personal retirement goals, providing you with a secure financial future.