If you’re looking to back ambitious, early-stage companies in the UK, there’s a particularly powerful incentive that can cut your tax bill – EIS tax relief.

Short for the Enterprise Investment Scheme, EIS tax relief offers an enticing combination of income tax breaks, potential exemption from capital gains tax (CGT) and more – if the company succeeds. While, if your chosen business fails, there’s also some downside protection with income tax relief for losses.

EIS tax relief is certainly complex, with various qualifying criteria that need to be met to unlock these tax breaks and claim relief. It’s a scheme definitely not for novice investors, but, for experienced investors prepared to take on a good amount of risk, the tax incentives are extremely generous.

What is EIS tax relief?

The Enterprise Investment Scheme, or EIS, was introduced in 1994 to help small, often young and ambitious businesses raise much needed finance by making them more attractive to individual investors. In effect, the scheme lowers the financial risk for investors prepared to invest in higher-risk small businesses that, if successful, could offer potentially substantial long-term growth – alongside doing their bit to support Britain’s economy. EIS can be an attractive proposition, as small businesses account for about 60% of employment and 50% of turnover in the UK private sector.

How EIS works

To claim EIS tax relief, you’ll need to invest directly in the ordinary shares of qualifying small UK companies not listed on a recognised stock exchange. It must be a new share issue – you cannot buy from someone else and benefit. Each year you can invest up to £1 million in EIS-qualifying shares and be eligible for income tax relief (£2 million if at least £1 million is invested in “knowledge-intensive” companies). That said, HMRC state, there can’t be an arrangement when the shares are issued to protect your investment, allow for a sale, structure activities to offer you undue benefit, or enable a reciprocal agreement where the company’s owner invests back in your business to gain tax relief. These stipulations essentially prevent exploitation of the EIS, by trying to ensure it truly serves a purpose beyond gaining tax relief, without genuine commercial intention.

It’s worth being aware of EIS’s little sibling too, the Seed Enterprise Investment Scheme or SEIS, aimed at even earlier-stage companies and offering investors even bigger tax incentives to invest in even higher risk businesses. For example, with SEIS, investors are given an upfront 50% income tax relief (with EIS it’s 30%), for up to £100,000 of SEIS investments made each tax year.

France, after noticing how well these UK schemes have worked to encourage individual investors to back small companies, decided to introduce their own versions. As the saying goes – imitation is the highest form of flattery. The new rules, due to take effect in 2024 and 2025 will mean, investors in what’s being termed deep tech startups get a 50% tax break for up to €100,000 in investments each year. And those investing in other, earlier stage, qualifying startups, can claim a 30% tax break for up to €150,000 invested each year.

Need professional assistance?

Sleek can assist you in applying for advance assurance from the government to validate these tax benefits. We manage the entire process, reducing administrative burden and stress, while offering expert advice. Make an enquiry today to see how we can support your investment journey.

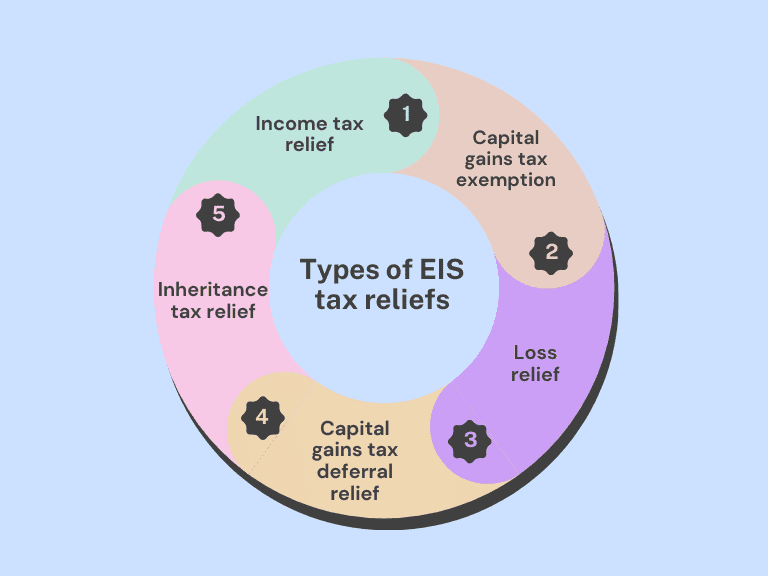

Types of EIS tax relief for investors

Income tax relief

For investors prepared to put money into EIS-qualifying shares, perhaps one of the most attractive potential benefits is up to 30% income tax relief. You can choose to offset it against the Income Tax you owe for the tax year when the investment is completed, or you can elect to offset against the previous year’s tax liability – which essentially means getting back tax already paid to HMRC. You’ll just need to have submitted your Self-Assessment Tax Return for that tax year.

Capital gains tax exemption when you sell your EIS investment

There is no Capital Gains Tax on the increase in value, if you’ve received EIS tax relief on your investment – provided it has not been withdrawn at a later date. Also you must have held the shares for at least 3 years – that’s known as the minimum qualifying period. Social Investment Tax Relief (another government scheme, for investments made before 5 April 2023) also exempts gains made, if qualifying criteria are met. Likewise, if you invest in a VCT (Venture Capital Trust) you will also avoid paying Capital Gains Tax, regardless of whether you invested in new or second-hand shares.

Capital Gains Tax reinvestment relief when you buy EIS shares

When you sell assets that don’t qualify for EIS, SEIS or SITR tax breaks and choose to reinvest all or part of any gains in shares that qualify for EIS relief, you’re given the option to defer the tax due on that gain. You must make the EIS investment within one calendar year before or up to 3 calendar years after selling those assets, regardless of whether you have any connection with the company (eg an existing shareholder, employee or director).

For example, you could reinvest the gain from selling shares in one company, in a different one that qualifies for EIS tax relief. A word of warning, there are various stipulations that define whether you are considered to be ‘connected’. See an example of how this deferral relief works on this gov.uk page. You’ll have to pay the capital gains tax if, at some point, you sell the EIS investment or the company stops meeting the EIS qualifying conditions. It also becomes due, if the investment is repaid to you or you leave the UK and are no longer tax resident.

Loss relief

As an investor in a qualifying EIS company, if you decide to sell your EIS shares and they have gone down in value – in other words you make a loss, then EIS tax relief comes with an additional safety net – income tax relief for those losses. You can choose to offset this amount, after deducting any income tax relief already given, against either the tax year your shares were sold or the previous tax year. With income tax currently at a high, that’s not to be sniffed at.

Which companies qualify for EIS?

A company, to be approved for EIS has to jump through many HMRC hoops to prove its EIS qualifying status – both for new and ongoing investments. You’ll see, for many EIS opportunities that investors are able to apply for Advance Assurance from HMRC, which means that in principle a particular company and share issue will likely qualify for EIS.

As HMRC is particularly overloaded these days with applications, it could be advisable to ensure this is the case before applying, if investing with the view of claiming those all-important tax breaks. But remember, as it’s a long, drawn out bureaucratic process, even having Advanced Assurance from HMRC should be read with a pinch of salt, as nothing is set in stone. It only covers the company qualifying and not the individual investor – investors still need to be sure to check their own personal qualifying status.

Broadly, companies applying for EIS must show genuine commercial intention and the potential for substantial growth. Some key EIS qualifying criteria companies must demonstrate are that:

- They have been trading for less than seven years

- They have fewer than 250 full-time employees

- Gross assets are less than £15 million

HMRC has full guidance for both investors and the companies themselves on the various conditions that must be met before claiming relief becomes possible. Although the company must have completed at least four months of trading to be able to apply, HMRC may also choose to visit businesses during the process, to ask various questions about how they’ve met EIS criteria.

Some sectors do not qualify for EIS, for example energy generation, farming, financial activities, property development and companies dealing in land. Certain community energy organisations have had funding under the VCT and social investment tax relief scheme, curtailed as of November 2015. As government schemes and their guidelines frequently change, please ensure you check current rulings and make sure you consult a financial adviser to clarify these complex issues.

The three-year rule

You must keep all the qualifying shares you invest in for at least three years to claim all the various EIS tax reliefs. Any EIS benefits already received can be withdrawn, if you dispose of some or all of the shares in that time or the company stops meeting EIS rules. Another factor is that the investor and company must remain unconnected during the entire three years – a complex and wide-ranging topic, so ensure you have expert financial advice to avoid any unexpected pitfalls. It could also affect the amount of EIS relief if money invested is paid back by the company to other investors who did not receive tax relief – but with EIS this stipulation only applies to investments made in the 12 months before you invested. If you’re considering SEIS or SITR, the rule is much stricter – it applies from when the company started trading.

Claiming EIS tax relief

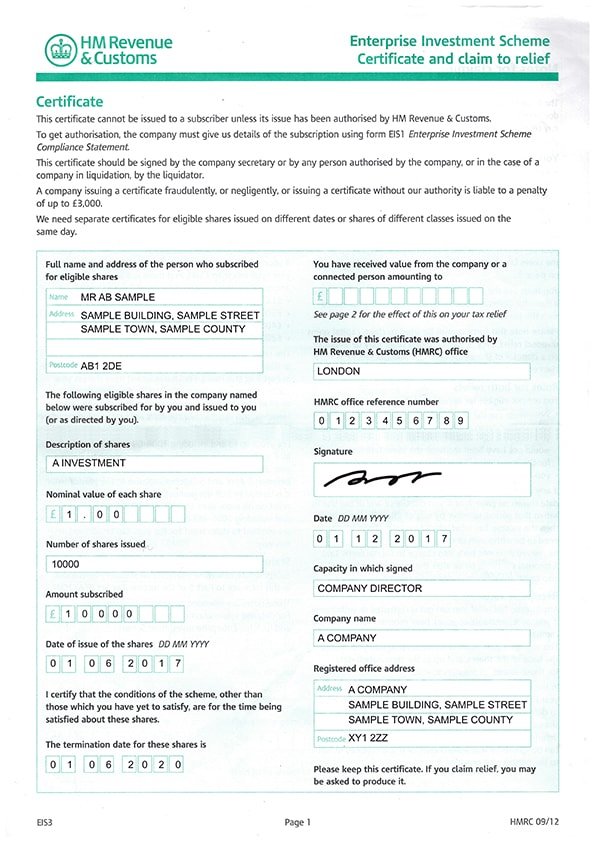

To be able to claim tax relief from HMRC under EIS, after you’ve made an investment in a company, you must wait for a Compliance Statement – sometimes called an EIS3 certificate or Form EIS3 – sent by the company to show the investment meets all the conditions of EIS and that, in theory, this should continue to be the case for three years. You’ll need this EIS certificate to claim both income tax and capital gains tax deferral relief. However, investors should be aware that although it’s standard for EIS managers and the companies themselves to specify expected deployment dates, the timing of issuing the EIS3 certificate by the company or its agents is out of their hands. For any income tax relief claim it may take 6 months (often much longer), but if it’s a claim for Capital Gains Deferral Relief, you might have to wait much longer for that magic piece of paper.

If your investment is through an ‘EIS Knowledge Intensive Approved Fund’ you’ll find you don’t receive an EIS3 but are sent an EIS5 compliance certificate from the fund manager. See an example of an EIS3 certificate ». Your EIS5 should list all your EIS Knowledge-Intensive investments with that manager.

This certificate doesn’t automatically qualify you for tax relief under EIS as, you as the investor also must meet the conditions of the scheme to be able to claim the relief from HMRC. If everything stacks up, here’s where to claim your tax relief:

- Claim income tax relief against the current tax year you make an investment in by changing your PAYE tax code.

- Claim income tax relief on your investments by completing an “Additional information” form SA101 and enclosing it with your tax return.

- Make your claim for relief from a previous year on your self-assessment tax return form.

Who cannot claim EIS tax relief

Tax Relief from EIS is restricted or unavailable in several scenarios. These are wide-ranging, covering whether you qualify as a UK taxpayer (being tax resident for example, or domiciled in the UK) or whether the shares were issued before you became connected with the company. You cannot claim if, for example:

- You’re employed by the company. As mentioned earlier, the ‘connection’ with the company is complex and covers various conditions (read the HMRC definition here), and includes unpaid directors, although this does not include those termed ‘business angels’.

- You hold more than 30% of the company shares.

- You and your associates hold more than 30% of rights to company assets if the business stops operating.

- The investment was made using a loan and was specifically for buying the EIS shares.

Claiming EIS relief if you’re a company director

For company directors, whether relief is available depends on several conditions:

Scheme | Can directors claim EIS relief?

|

|---|---|

Seed Enterprise Investment Scheme | You can claim EIS relief if you’re a director of a SEIS qualifying company, paid or unpaid. |

Social Investment Tax Relief | You can’t claim EIS relief if you are paid as a company director for a qualifying social enterprise. However unpaid directors are eligible for the scheme. |

Enterprise Investment Scheme | You can’t claim if you’re a paid director at the point when the company issues the shares unless the payments meet HMRC’s specific ‘permitted payments’ definition, available here. You may be able to claim, if when the shares were issued you:

|

Importantly, directors who receive upfront Income Tax relief can keep that relief should they go on to be paid. There is also the possibility to claim further tax relief once becoming paid, under EIS, but only if you originally invested before the company started to pay you – providing this is either within 3 years of those original shares being issued or the point when the company started to trade. Another situation is that as an unpaid company director you invested in SEIS shares and received Income Tax relief and those further EIS share investments are also within three years of the original share investments you made in the SEIS company.

Claiming EIS Relief for joint investments

If shares are held in joint names (eg partners, spouses), it’s worth noting that EIS rules treat both parties as subscribing the same amount. To illustrate this further, if you and your spouse make an investment of £20,000 and receive 20,000 shares, both parties are treated as investing £10,000, irrespective of how much each person actually contributed. To claim EIS relief in that situation, HMRC requires each joint owner of shares to get their own EIS3 compliance certificate directly from the company. The HMRC self-assessment helpsheet covers this scenario in more detail.

What could disqualify a company from EIS?

It’s also worth considering that even when the initial investment round meets all HMRC EIS qualifying conditions, if any stipulations change in those crucial first 3 years after the investment, you as the investor will not be able to claim the upfront income tax relief. You must notify HMRC if any of these happen:

- Your EIS shares, or a proportion, are sold.

- There’s a connection (such as employment) between you, or an associate and the company. Note the definition of ‘associate’ is broad, including spouses, children, business partners, trustees of settlements where you’re the beneficiary etc.

- The company’s EIS status is revoked by HMRC.

- There’s unusual or high levels of interest on any company loan received.

- The company is bought by a bigger one.

- Assets (including cash) are received by you or your associates.

Conclusion

EIS tax relief offers significant benefits for investors willing to support early-stage and intensive companies. Although it may not suit every investor, those with a long-term perspective and a high risk tolerance may find the Enterprise Investment Scheme to be a valuable incentive. Given the complexity and frequent changes in the rules governing venture capital schemes, it is crucial to avail professional guidance. This will help you fully understand all aspects of EIS tax relief and determine if it is the right investment strategy for you.

The EIS is designed to help businesses grow by providing investors with tax relief, thereby reducing the risk associated with investing.

Easily apply for advance assurance with Sleek and validate your EIS tax benefits. Our seasoned experts will handle the entire process, reducing administrative burden and stress while providing you with the guidance you need. Make an enquiry today to see how Sleek can support your investment journey.

FAQs about EIS tax relief

How does tax relief work on EIS?

Investors who make a qualifying investment in an EIS-approved company can claim several tax reliefs. Income Tax relief can be claimed of 30% (on a maximum of £1 million invested) in the year the investment is made. Any gains from a future sale of shares (after the minimum three years qualifying period) are exempt from capital gains tax. If you make a loss, this can be offset against income. EIS investments also potentially qualify for Business Property Relief (BPR), which can offer exemption from Inheritance Tax, if conditions are met. You must keep all shares for the minimum 3 year qualifying period to be eligible for EIS benefits.

Can you offset EIS losses against income tax?

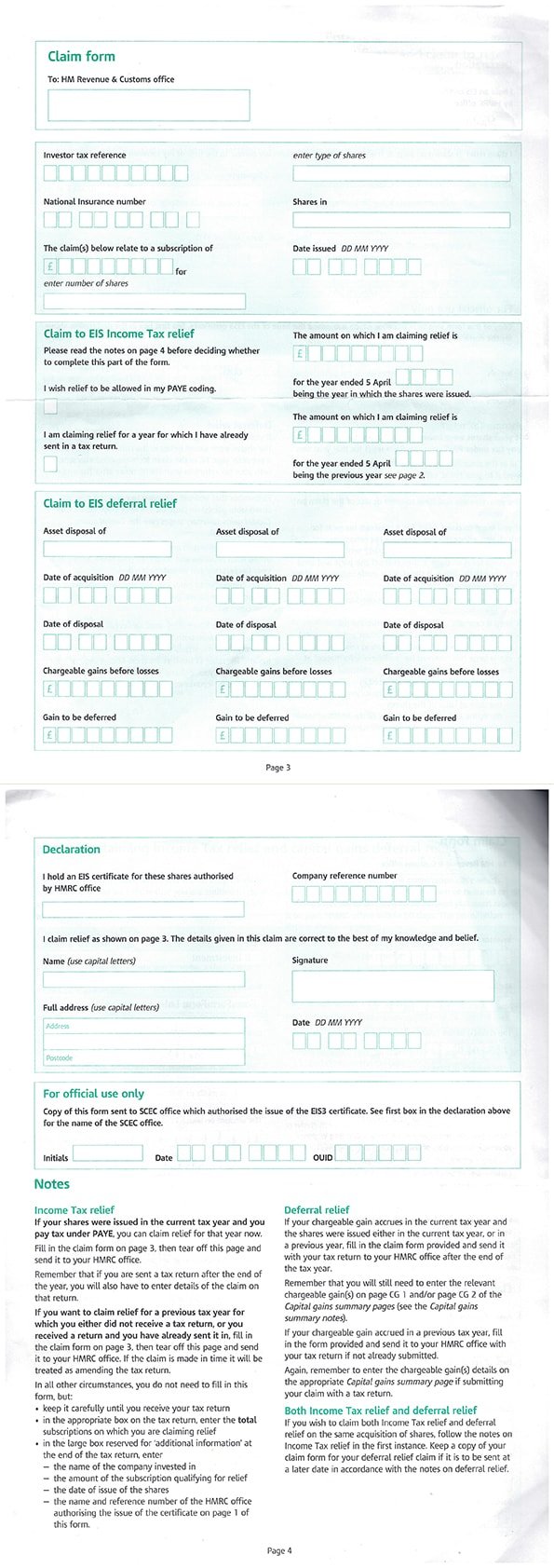

This is one of the key benefits of EIS tax relief. Investors who have sold shares at a loss in an EIS-approved company (after claiming 30% income tax relief) are able to choose to offset those losses against income tax liability, providing further protection to your original investment amount. See an example of EIS claim form ». You can choose to offset those losses against the income tax liability either for the year in which the EIS investment was sold or for the previous tax year.

How does the EIS work?

Essentially, the UK Government, using a range of generous tax benefits, encourages individuals to invest in early-stage small, high-growth potential, unquoted trading businesses, with the incentive being a reduced investment risk – for qualifying investments. This is beneficial to the investors, the businesses raising capital and helps to support the UK economy, by providing extra funding and confidence in this important market. To encourage transparency and make sure schemes like EIS aren’t misused or open to exploitation, various complex criteria have been set in place by HMRC. This essentially involves a good deal of ‘red tape’ – ensuring that investments meet qualifying criteria, the company operates according to specific conditions and continues to do so over the qualifying three year period. It’s definitely advisable to ensure all parties – the company, the investor and all their investments and payments meet HMRC’s criteria before proceeding. The Enterprise Investment Scheme Association, covers EIS in detail on its website.

What is the three year rule for EIS?

Investors in qualifying companies who have claimed income tax relief on their EIS investment (which, with EIS is 30% of the investment amount), to be able to retain all those generous tax reliefs must adhere to the qualifying period for EIS – that is, holding all those shares for at least 3 years from the date those shares are issued. If in this qualifying period, either the investor (or anyone directly associated with the investor) become connected with the company, any of the shares are disposed of, the company loses its qualifying EIS status or stops trading, or even receives funds back from other qualifying investors, the investor will be required to either partially or even fully repay any EIS tax relief.

450,000

businesses worldwide.

from 4,100+ reviews.

satisfaction rate from

16,000 surveyed clients.

{kind=link}

{kind=link}