Dividend allowance: Maximise your tax-free income

Working hard, yet feeling like taxes are constantly chipping away at your bottom line? Whether you’re a contractor, sole trader, startup founder, or limited company director, the dividend allowance provides a lifeline. It’s a chance to shield some of your income from taxation, helping you keep more earnings.

Imagine having extra funds to reinvest in your business, build your savings, or simply enjoy the fruits of your labour. Understanding the dividend allowance is the first step towards unlocking those possibilities.

This guide breaks down the rules, gives you actionable strategies, and helps you confidently navigate your tax obligations to maximise this powerful financial tool.

What is dividend allowance?

Dividend Allowance is a tax-related concept that refers to an individual’s dividend income each year without paying taxes. Essentially, it serves as a tax-free threshold for dividends.

Introduced in various jurisdictions with different rates and rules, this allowance allows investors who receive dividends from shares they own in companies not to be taxed on all their dividend income.

For instance, the UK, the government sets a specific Dividend Allowance, which has changed over recent years. Individuals could earn up to a certain amount in dividends within the tax year before any tax would be payable.

Amounts above this threshold are then taxed at graduated rates depending on one’s total taxable income and thus fall into different tax bands—basic rate, higher rate or additional rate.

How do dividend allowances work?

The Dividend Allowance is the income from dividends that an individual can earn before tax is incurred. For the 2024/25 tax year, the Dividend Allowance is £500. You can find more information about the Dividend Allowance on the government’s website. This allowance is available to all taxpayers, regardless of the rate at which they pay tax.

Annual dividend allowance limit

Notably, the dividend allowance for the 2023-2024 tax year is £1,000, which will be cut to £500 from April 2024. This is in addition to your personal tax allowance, which is £12,570 this tax year and can be used if your only income is from investments.

How is dividend income taxed?

Once you’ve used up your Dividend Allowance, any additional dividend income you receive will be subject to dividend tax. The rate at which you pay tax on your dividends depends on your tax band, also known as your “marginal rate.” Let’s take a closer look at the different rates.

1. Basic rate dividend tax

If your total income tax rate, including dividends, falls within the basic rate tax band (up to £37,700 for the 2024/25 tax year), you’ll pay a dividend tax rate of 8.75% on dividends above your allowance.

2. Higher rate dividend tax

For those whose income falls into the higher rate tax band (between £37,701 and £125,140 for the 2024/25 tax year), the dividend tax rate jumps to 33.75% on dividends above the allowance.

3. Additional rate dividend tax

If you’re an additional-rate taxpayer with income exceeding £125,140, you’ll face a 39.35% tax rate on dividends above your allowance.

Calculating your dividend tax

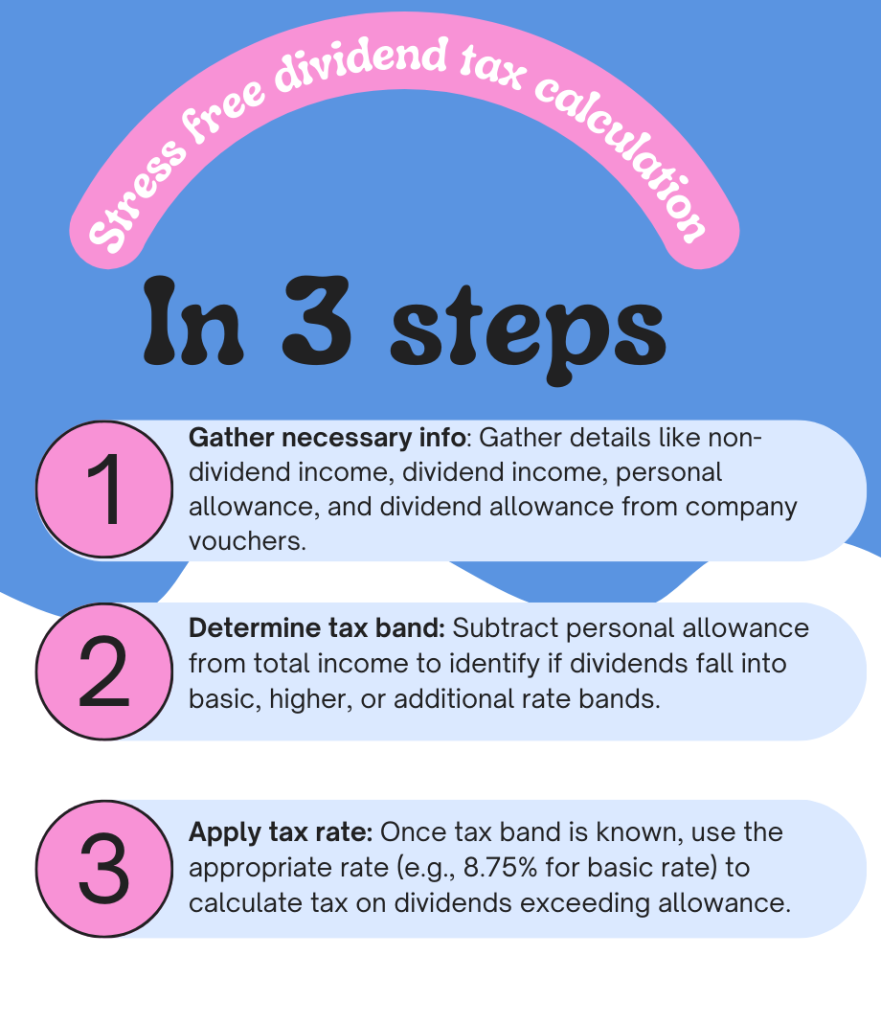

Now that you understand the basics of dividend allowances and tax rates, let’s discuss how to calculate your dividend tax liability.

1. Gathering necessary information

To calculate your dividend tax, you’ll need to gather information including your non-dividend income, dividend income, personal allowance, and dividend allowance for the relevant tax year. Dividend vouchers from each company you hold shares in will detail the dividend payments you’ve received.

2. Determining your tax band

After deducting your personal allowance from your total income, you can determine which tax band your dividends fall into – basic rate, higher rate, or additional rate. The tax band your dividends fall into will determine the tax rate applied to dividends above your allowance.

3. Applying the appropriate tax rate

Once you’ve determined your tax band, you can apply the appropriate dividend tax rate to your dividends above the allowance. For example, if your dividends above the allowance fall within the basic rate band, they will be taxed at 8.75%. The tax payable is calculated by multiplying the dividends above the allowance by the relevant tax rate percentage.

Dividend allowance and other income sources

Understanding how the dividend allowance interacts with other types of income and allowances is essential for optimizing your tax strategy.

Interaction with the personal allowance

The dividend allowance is in addition to your personal allowance, which is £12,570 for the 2023/24 tax year. Your personal allowance is first applied to your non-dividend income, such as salary or rental income. Any remaining personal allowance can then be set against your dividend income.

Impact on savings allowance

Your dividend allowance is separate from your Personal Savings Allowance. The Personal Savings Allowance allows basic rate taxpayers to earn £1,000 in savings income tax-free, while higher rate taxpayers can earn £500. Additional rate taxpayers do not receive a Personal Savings Allowance.

Relation to Capital Gains Tax

Dividends are considered income for tax purposes and are not subject to Capital Gains Tax. Capital Gains Tax is a separate tax that is charged on the profit when you sell or dispose of an asset that has increased in value. The dividend allowance does not impact your Capital Gains Tax allowance.

Strategies to maximise your dividend allowance

Now that you have a solid grasp of how the dividend allowance works, let’s explore some strategies for maximizing it and minimizing your tax liability.

1. Utilizing ISAs for dividend income

Investing in dividend-paying shares within a Stocks and Shares ISA allows you to receive dividend payments tax-free, as they do not count towards your dividend allowance. The annual ISA allowance for the 2023/24 tax year is £20,000, which can be split between different types of ISAs.

2. Spreading dividends across tax years

If you own a company and have flexibility over when to pay dividends, consider spreading dividend payments across tax years to make the most of your annual dividend allowance. Delaying a dividend payment until the start of a new tax year could help you utilize two years’ worth of allowances.

3. Reviewing your tax code

Ensuring your tax code is correct can help you maximize your dividend and personal allowance. If you receive dividends from shares outside of an ISA, HMRC will usually adjust your tax code to collect any tax paid on dividends above the allowance. Reviewing your tax code and contacting HMRC if it appears incorrect can help avoid overpaying or underpaying tax.

Dividend allowance for Scottish taxpayers

While the dividend allowance and dividend tax rates are the same for all UK taxpayers, Scottish taxpayers may have different income tax bands and tax rates than taxpayers in the rest of the UK.

For the 2023/24 tax year, the higher rate income tax threshold for Scottish taxpayers is £31,092, compared to £37,700 for taxpayers in the rest of the UK. This means Scottish taxpayers may pay the higher dividend tax rate sooner than taxpayers elsewhere in the UK.

Reporting dividend income on your tax return

You may need to report dividends on a self-assessment tax return if you receive them outside of an ISA. You’ll need to report the total dividends received, even if they fall within your dividend allowance.

If your total dividend income falls below £10,000, you can contact HMRC and ask for your tax code to be adjusted to collect any tax due. However, if your dividend income exceeds £10,000 or you receive other untaxed income, you’ll need to complete a Self Assessment tax return.

Key Takeaway:

Get smart with your dividend allowance to pay less tax. Invest in ISAs, time your dividends right, and always check your tax code. It’s not just about knowing the rules; it’s playing them well.

Conclusion

So there you have it. The lowdown on the dividend allowance and how to make it work for you. It’s about knowing what it is and how to use it to your advantage.

Remember, the dividend allowance is your ticket to earning tax-free income from your investments. By spreading your dividends across tax years, using ISAs, and keeping an eye on your tax band, you can maximise your allowance and keep more money in your pocket.

Don’t be afraid to chat with a tax pro or financial advisor for personalised guidance. A great choice is Sleek – a digital platform dedicated to small businesses. Their seasoned professionals can help you navigate the ins and outs of the dividend allowance and create a strategy tailored to your unique needs.

FAQs in relation to dividend allowance

What is the UK dividend allowance?

The dividend allowance is the amount of dividend income you can receive each tax year tax-free. For the 2024/25 tax year, it’s £500. Any dividends over this amount are taxed at your specific dividend tax rate.

Who is eligible for the dividend allowance?

Anyone who receives dividend income from shares in UK companies is eligible, including:

- Company directors

- Shareholders

- Sole traders (consider it part of your overall personal allowance)

- Contractors operating through limited companies

How does the dividend allowance affect my taxes?

It directly reduces your taxable income. If your dividends fall within the allowance, you don’t pay additional tax on them. Dividends exceeding the allowance are taxed at rates based on your income tax band.

Are dividends from ISAs included in the allowance?

No! Dividends from an ISA are always tax-free and don’t affect your dividend allowance.

Can I carry forward unused dividend allowance?

Unfortunately, no. The dividend allowance is a “use it or lose it” benefit within each tax year.